From May 1st, 2026 France’s Contract for Difference (CfD) mechanism for renewables is entering a new phase, with updated rules governing downward production modulation. Here is a closer look at what this means for renewable producers and how it ripples through energy markets.

Note: This mechanism is complex and involves several special cases. I have deliberately simplified certain aspects to illustrate the core principles rather than every technical detail. For a deeper dive into edge cases and specifics, feel free to reach out directly.

In the era of full subsidies, renewable producers operated under a single directive: maximise output at all times, regardless of market conditions. This “always-on” approach served its purpose it fueled the rapid growth of the renewable sector but it became increasingly untenable as renewable capacity grew large enough to materially affect the supply-demand balance.

To move away from this inefficiency, CfD-supported renewable plants were given a new incentive: curtail production during periods of negative spot prices. The mechanism works as follows:

- When spot prices turn negative, producers who curtail receive a premium calculated on the basis of their deemed production i.e. what they would have generated had they continued operating.

- Operationally, this is straightforward to implement via day-ahead linear orders: producers and their aggregators can structure their bids to sell only when prices are positive, effectively automating the curtailment decision for each settlement period.

Problem solved? Only partially.

A challenge for TSOs

When all CfD-supported renewables respond to the same price signal and curtail simultaneously, TSOs face abrupt multi-gigawatt power swings within a matter of minutes. Managing these ramps requires activating aFRR and mFRR reserves balancing mechanisms that themselves take 5 to 15 minutes to deploy.

Up to now, as CfD negative price windows were settled hourly, TSOs could manage these fluctuations with reasonable effort. The CfD imminent switch to 15-minute will dramatically compress response windows, intensifying the challenge and driving the introduction of new modulation rules.

Across all TSOs, this creates a threefold challenge:

- Ensuring renewable producers have a genuine incentive to submit accurate production schedules

- Calibrating the depth of curtailment to the severity of the price signal

- Avoiding synchronised curtailment across the entire renewable fleet

First challenge: production schedules

Renewable energy producers are legally required to submit their best estimate of their production schedule, as are all other market participants. Yet in practice, these schedules carry limited financial consequences: only imbalances settled through the BRP mechanism are directly affected by forecast errors. This weak incentive structure is precisely why RTE has signalled an intention to introduce penalties for deviations between scheduled and realised production, expected around 2027, though nothing is yet in force.

Second challenge: calibrating curtailment depth to price signals

In principle, curtailment decisions should scale with the depth of negative prices — the more negative the signal, the stronger the incentive to reduce output. To approximate this, a buffer price window was introduced: within the [-0.1 €/MWh; -0.01 €/MWh[ range, producers receive the negative price premium whether they curtail or continue producing. In practice, however, the measure has had little discernible effect on producer behaviour.

A revised set of rules has therefore been put in place to sharpen producer incentives during these buffer windows.

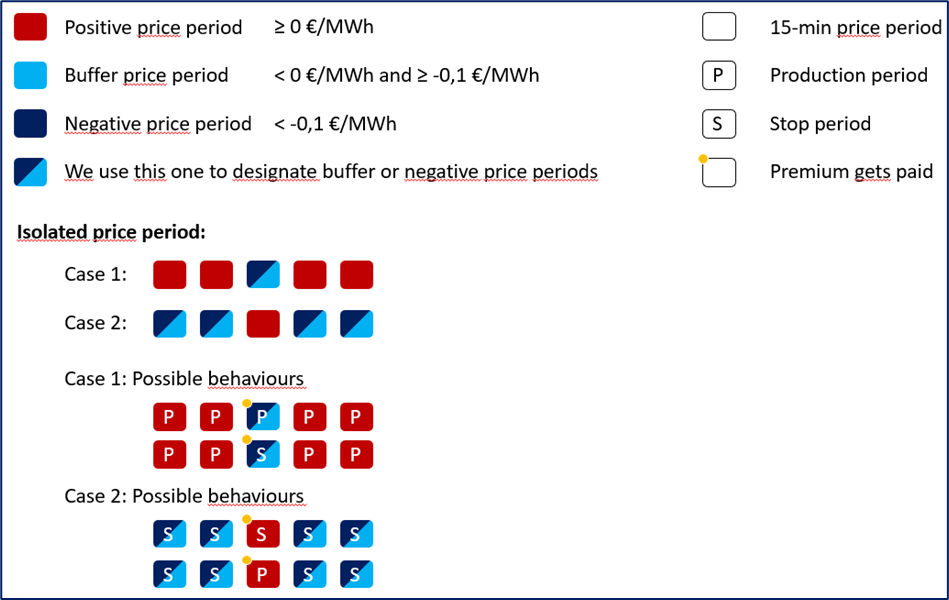

The negative prices isolated periods rule

- For an isolated negative-price 15-minute window, producers receive the negative price premium regardless of whether they curtail or continue producing.

- Symmetrically, for an isolated positive-price 15-minute window surrounded by negative-price periods, producers also receive the negative price premium regardless of output but the CfD top-up is not paid for that period.

- Since starting and stopping a plant carries real O&M costs whether immediately or over time removing the financial incentive to act on isolated price periods should naturally discourage unnecessary cycling.

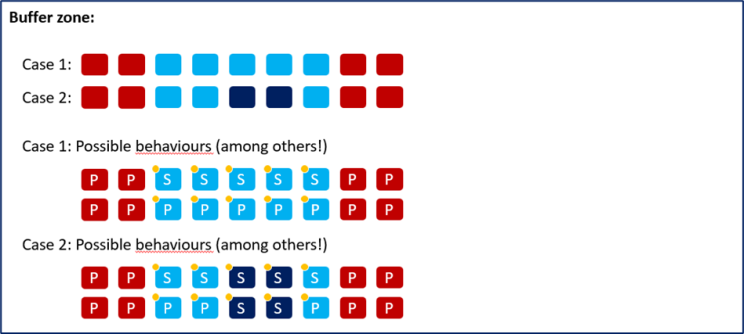

The improved buffer zone principle

- In practice, this buffer zone appears frequently most often at the entry and exit points of deeply negative price episodes.

- By giving producers discretion over whether to curtail during these periods, the rule naturally staggers their decisions reducing the risk of a cliff-edge, synchronised ramp-down.

Third challenge: Prevent all renewable producers from curtailing simultaneously

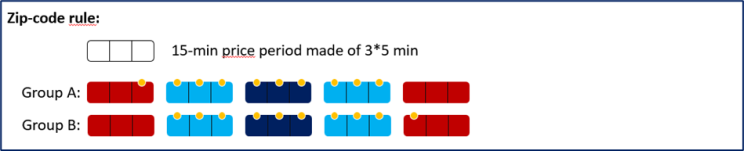

The zip-code rule

Even with the buffer zone in place, producers within the same cohort may still react identically applying the same curtailment logic at the same moment. The zip-code rule is designed to break this residual synchronisation.

The mechanism rests on one of mathematics’ most reliable properties: every integer is either even or odd.

Two groups are created accordingly. Group A covers “facilities for which the sum of the five digits making up the postcode linked to the establishment identification code of the production site, as indicated on the certificate of registration in the National Business Register, is even.” I let you guess what Group B covers.

Group A accounts for approximately 56% of total renewable installed capacity in France leaving Group B with the remaining 44%. A roughly balanced split, as intended.

How does this translate into market behaviour?

- Group A plants are incentivised to begin ramping down during the last 5 minutes of the period preceding the first period where the negative price premium starts applying. During those 5 minutes, the CfD is not paid; the premium is paid only if a ramp down is observed.

- Group B plants are incentivised to begin ramping down during the first 5 minutes of the first period where the negative price premium starts applying. During those 5 minutes, the premium is paid only if a ramp down is observed.

- Group A plants are incentivised to begin ramping up during the last 5 minutes of the last period where the negative price premium applies. During those 5 minutes, the premium is paid only if a ramp up is observed.

- Group B plants are incentivised to begin ramping up during the first 5 minutes of the first period following the last period where the negative price premium applies. During those 5 minutes, the CfD is not paid; the premium is paid only if a ramp up is observed.

This is also designed to align renewable curtailment windows with EU regulation (“control program calculation” Art. 136 of European System Operations Guidelines).

Notably, these rules collectively introduce and entrench an additional layer of granularity in how the French CfD market operates: the 5-minute time step a level of precision that will increasingly shape how producers, aggregators and market participants model and optimise their positions.

Conclusion

The new CfD modulation rules — isolated periods, buffer zones, zip-code groupings, 5-minute ramp windows — are undeniably complex. But that complexity is not arbitrary: it reflects the fundamental friction that arises when contractual support schemes, market price signals, and hard physical grid constraints are forced to coexist at scale. Each new rule is, in essence, a negotiation between what the contract promises, what the market says, and what the grid can physically absorb.

And this is only part of the picture. I have deliberately left aside one further consequence of these new rules: by granting producers flexibility over whether to produce during buffer zones and isolated price periods, the framework quietly disrupts the relationship between renewable producers and their Balance Responsible Parties. That flexibility, welcome as it is, creates uncertainty in production forecasts that will need to be reflected in contractual arrangements between producers and their BRPs. Revisions ahead.

There is also a subtler but potentially significant market structure implication. Once producers can legitimately choose not to produce during certain price periods — irrespective of the sign of the price — the classic linear order in day-ahead auctions begins to show its limits. Block orders, which allow participants to condition acceptance of a bid on a set of consecutive periods rather than each period individually, are equally ill-suited: their price condition applies to the block as a whole, not to individual sub-periods. The new rules therefore expose a genuine gap in the available suite of bidding instruments, and a clear need for purpose-built market products to fill it.

The current rules are not an endpoint. They are the first chapter of a much longer adaptation — one that will reshape how renewables are contracted, balanced, and traded as the energy transition moves from ambition to infrastructure.

A whole new chapter ahead (and new headaches!), indeed.

Navigating CfD modulation rules, zip-code groupings and 5-minute ramp windows is exactly what Xtra-energy’s platform is designed for. We help renewable producers turn regulatory complexity into revenue performance.

Comments are closed